This blog focuses on the Interest Rate system. We will try and answer the questions like – What does the Interest rate landscape look like? What is the basis of deciding the rate of interest? Is interest rate connected to investment risk? What are the products available starting from low interest to high interest and which one should you invest in?

Believe me that this article is not written to improve your knowledge. But I am here to give you practical and simple Investment Ideas. You can quit reading my articles in case you don’t find practical value. And I am sure you will not waste a moment in deciding on that.

My ‘Interest’ is ‘Rate of Interest’

You have a beautiful residential flat in prime locality and wish to rent it out. You will charge the rent as per the standard rates in that locality. Similarly, if you wish to rent in a shop in a commercial complex; you will have to pay rent on your flat. When you book a hotel room on your tour to Mumbai, need to pay room charges.

In all above cases, either you are using someone else’s assets (flat or shop or hotel room) or you are giving your assets to someone else to use. Whenever an asset is used by another entity/person he/she will have to pay rent to the person owning the asset.

When money is given to someone else to use the ‘rent’ received on that money is called interest. For example, when you give your money to the Bank in the form of a Fixed Deposit (FD), the bank pays you the rent. This rent paid by bank for using your money (money is an asset) is ‘Interest’.

How is the Rate of Interest decided?

Deciding the interest rate is similar to how the price of any goods is decided. Repo Rate is the base interest rate decided by the Reserve Bank of India. Repo Rate is like the manufacturing price of shoes. Reserve Bank Of India offers loans to all Banks in India at interest rate equal to Repo Rate. Now, since banks have to earn some profit, they charge higher interest rates to their loan customers as compared to the Repo Rate.

Though above example is a simple way of expressing the Bank Interest Rate, there can be some more factors affecting the interest rate. What are these factors?

Various shoe brands have different prices for similar types of shoes. The price of these shoes depend on the quality and the brand value to which it belongs. Similarly the Rate of Interest that a Bank charges on Loan and the Rate of Interest that a Bank offers on Fixed Deposits also depend on various factors.

Single most important factor deciding the Interest Rate offered by any institution is the Credit Rating of that institution or the Bank. Credit rating is nothing but assessment of the ability of the person to repay the borrowed money.

Individuals, Companies, Banks and even the Governments are ‘Rates’ by different rating agencies. All of us know CIBIL is one such credit rating agency which assesses the Credit Rating of Individuals. There are some other rating agencies which assess the credit rating of companies and banks. There are some international rating agencies which assess the rating of the governments.

I will be shortly coming up with an article on the Credit Rating system.

Credit Rating

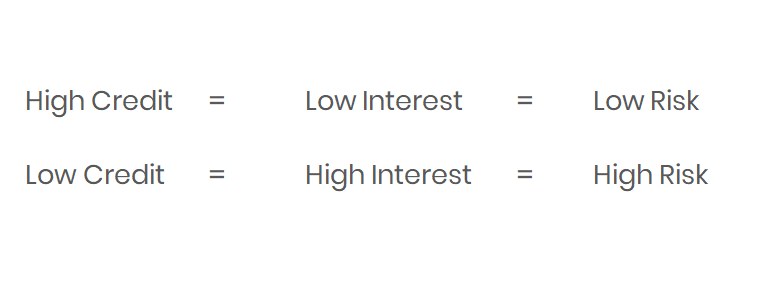

As a general rule and of course as a common sense, higher the credit rating of an individual or a bank higher are the chances that the individual (or the bank) will return your borrowed money. So we can conclude that higher the credit rating of the borrower, lower the risk of the lender. This is because an individual or entity with a high credit rating is expected to return the borrowed money in time. Vice versa is also true. Lower the credit rating of an individual, less are the chances of him returning the borrowed money and hence higher is the risk.

We understand following points from the above equation.

If you deposit your money in banks with higher credit ratings, you will get a low rate of interest but your money will be safe. As you move to lower credit rated banks, you will get a higher rate of interest, but risk to your money increases.

Now you can understand why a bank like State Bank of India which is rated high will offer you a low rate of interest. But at the same time your money will be safe with banks like SBI. If you go and invest in FDs of some smaller private banks or co-operative bank or cooperative credit societies, they will offer you higher interest, but you will be at high risk of losing your money.

As this equation is true with banks, it is true with any other institution borrowing your money. If you lend your money to a company (by buying their Bonds), the rate of interest you will get depends upon the credit rating of that company. You would have observed that the smaller companies (with lower credit rating) offer your high bond yield.

Equation

Based on this we arrive at equation shown in the following picture –

Now the question is – Which type of Investment option should I invest? With lower interest at great safety or higher rate of interest with high risk? The answer is – It depends on your priorities. We shall discuss this in more detail in a very simple manner in the next article.

Do let me know the topics which I should cover in my future articles. You can also mention / ask questions in the comment box below.

Get our blogs/articles delivered in your inbox. Click Here to subscribe.