All of us vouch for investment which gives better returns but at the same time returns should be assured. We all wish to have low risk and capital protection but high returns. There is one product which can fulfill all your wishes. The name of the product is Peer 2 Peer Lending or simply, P2P Lending.

In this article let’s understand more about P2P Lending.

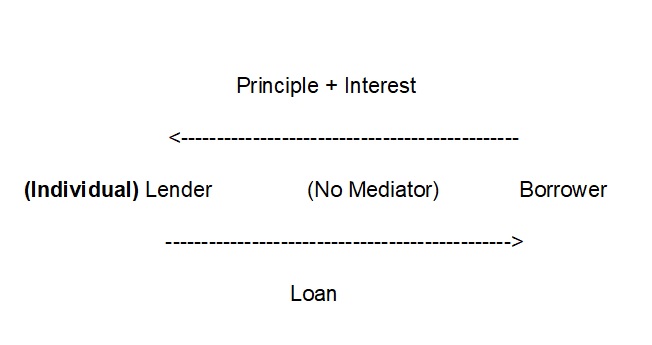

In private lending one person lends to another person based on some terms and conditions. Here, no third party is involved. The lender is responsible for recovering the basic amount and interest from the borrower. This process of management (recovery) is risky. Most individuals do not have willingness and bandwidth to get involved in these acts. However, the lender gets very high interest on the amount he lends.

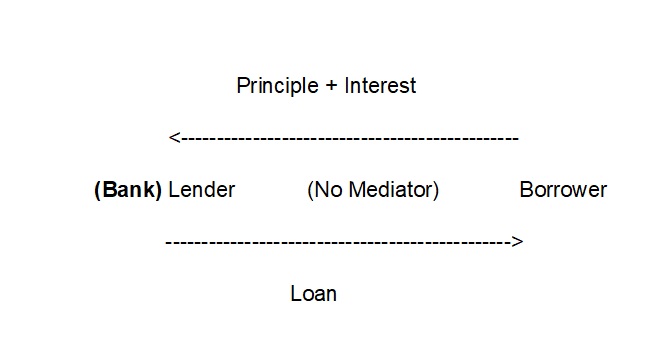

In case of a bank personal loan, the bank gives loan to an individual based on some terms and conditions. In this case the bank has a mechanism to manage the loans. The bank officials are responsible for the act of loan management. Banks also have recovery mechanisms in place. Here the bank enjoys the high interest it earns on personal loans.

P2P Lending is very similar to private lending or a bank loan.

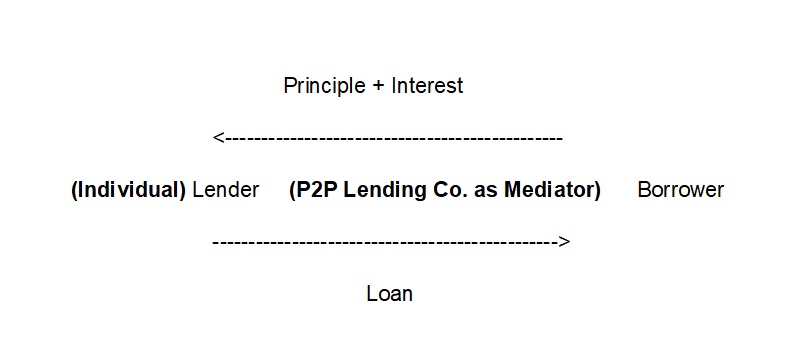

The name Peer to Peer lending suggests that it’s the loan given by one person to another person. Practically it is difficult for an individual to search for a borrower. Moreover, a lender may not be able to manage and keep all the accounting. Here comes the P2P lending company. P2P lending company unites lender and the borrower. P2P lending company does the end to end processing of the loan between these 2 parties. For their work, P2P lending company charges a small processing fee. The interest received from the borrower is passed on to the lender after deducting the processing charges. Thus the lender enjoys a high interest rate on this personal loan.

You can see in the diagram above that you as an investor (lender) become a bank when you invest through P2P Platform. A bank lends money deposited by its depositors in instruments such as savings account or FD. Now a bank pays interest between 3% to 7% on saving account and FD. But it lends this money to a borrower at around 15% (personal loan rate interest is high). You can imagine the bank earns a difference of around 12% to 8% in this transaction. Here is the biggest advantage to you as an investor in case of P2P lending. In this case since there is no bank involved you as an investor earn the interest on the lending amount after deducting a small fee charged by the P2P lending platform.

The loans given through a P2P platform are Personal Loan. As you must be aware that Personal Loan rates of interest are very high. The interest ranges between 12% to as high as 30%. You as a lender (Investor) have potential to earn these returns. The returns are assured (not guaranteed) as the rate of interest on these loans is fixed. You can expect to make these hefty returns on the investment. The returns come back to you in the form of an EMI as in case of any loan. EMI has two components – Principle and Interest. In most of the cases you have flexibility to reinvest the interest. You may also reinvest (lend again) both components that are principal and interest.

P2P lending company runs the show. They unite the Borrower and the Lender through an online platform (a website or mobile app).

P2P lending company advertises the loan to the appropriate borrower who fits in the criteria. They do the job of thorough scrutiny of the borrower and then approve the loan. The loans are usually smaller in size (as compared to the bank loans). The loans are given for a shorter period of time which is usually between 12 months to 36 months.

P2P lending company accepts the deposits from the investors (lenders). This amount is kept in the escrow account. Then the amount is distributed among the borrowers appropriately. Usually the amount of one investor (lender) is distributed among many borrowers for safety reasons.

The P2P lending company does the job of accounting and transactions. They maintain all the data and provide account statements from time to time. P2P lending company is responsible for recovery of the amount from the borrowers. Usually they have the recovery mechanism as per the guidelines from RBI.

Any loan (loan is a kind of debt instrument) is associated with the risk of defaulting. In case the borrower does not pay back the amount he/she borrowed the lender can lose the entire or part of the capital (principle). This is termed as NAP (Non performing asset) in banking terminology.

Having said that, any debt investment (FD, Debt Mutual Funds, Bonds) is subject to the risk of default. You might have heard of some instances wherein some companies have not paid back the loan they have borrowed from banks or from the Mutual Fund companies in the form of Bonds.

Read: Asset Classes! What are they and what role do they play in your Investment

Similarly, in case of P2P there is risk of default. Neither RBI nor the P2P lending company guarantees the principle of the lender. However, even the banks are also subject to similar NPA when they lend out personal loans.

While there is risk of default, it does not mean that all the amount of the lender will be lost. Usually a good care is taken by the P2P lending companies to protect the capital of its investors. We shall discuss these mechanisms in later articles. In the short lived history of Indian P2P companies the default rate is between 0.5% to 3%. This means that the lender will lose only about 3% of its capital. But against that he earns the interest to the tune of an average 15%. After adjusting 3% default the net returns settles at 12%.

In India RBI approves the License of a P2P Lending Platform. This license is known as NBFC-P2P. You can check the P2P lending companies and their registration details here on RBI website.

RBI has strict guidelines while issuing NBFC-P2P license to an entity. Only in case the entity and its promoters fulfill the criteria such as below, the license is issued –